Loans have become a normal part of financial life—whether someone wants to buy a home, purchase a vehicle, fund higher education, or simply manage emergency expenses. Yet, despite how common borrowing has become, many loan myths still mislead people into making bad financial decisions.

These myths often come from:

✔ Friends

✔ Family

✔ Social media

✔ Outdated information

✔ Misunderstanding of how loans actually work

The problem?

Believing loan myths can cost you money, opportunities, and even your financial security.

This ultimate guide will uncover the most common loan myths people still believe, explain why they are wrong, and reveal the real truths you must know before applying for any loan.

📌 Why Loan Myths Are Dangerous

Loan myths may seem harmless, but they can lead to:

🚫 High-interest borrowing

🚫 Rejected loan applications

🚫 Bad credit score

🚫 Losing valuable collateral

🚫 Debt traps

Knowledge is your biggest financial weapon.

So let’s bust these common loan myths once and for all.

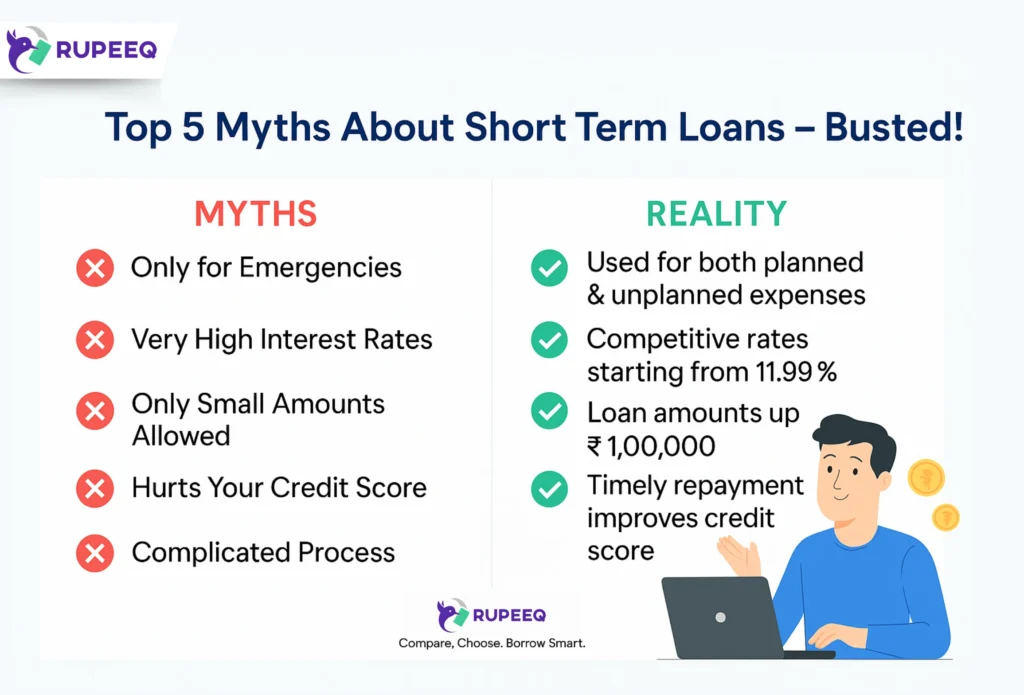

🧨 Myth #1: “Loans Are Only for People Who Don’t Have Money”

The Truth:

Even wealthy individuals and successful companies take loans — not because they are broke, but to:

✔ Grow their business

✔ Buy property as an investment

✔ Save tax

✔ Maintain liquidity (cash on hand)

Borrowing money strategically can help you multiply wealth.

Loans are a financial tool, not a sign of weakness.

🤯 Myth #2: “A Loan Will Always Ruin My Credit Score”

The Truth:

A loan itself does not hurt your credit score. In fact, taking a loan and repaying it on time can improve your score.

Your credit score increases when you:

✔ Pay EMIs before due dates

✔ Maintain low credit utilization

✔ Have a healthy credit mix (secured + unsecured loans)

Bad credit scores happen only when:

❌ EMI defaults

❌ Late payments

❌ Loan overborrowing

So loans are not the enemy — irresponsible repayment is.

🏦 Myth #3: “Every Bank Offers the Same Loan Terms”

The Truth:

Interest rates, processing fees, loan tenure, and eligibility criteria vary significantly between lenders.

Factors that change from bank to bank:

| Factor | Varies By Lender? |

|---|---|

| Interest Rate | ✔ |

| Loan Processing Fees | ✔ |

| Maximum Loan Amount | ✔ |

| Eligibility Rules | ✔ |

| Loan Tenure | ✔ |

| Prepayment Charges | ✔ |

Smart borrowers compare before applying — because one bank may cost you much more than another.

🔐 Myth #4: “Collateral Guarantees Loan Approval”

The Truth:

Collateral helps, but does not guarantee loan approval.

You still must meet background checks:

✔ Income stability

✔ Credit history

✔ Legal ownership of collateral

✔ Document verification

If any red flag appears, a lender may still reject the loan.

Collateral is a supporting factor, not an automatic passport.

🧾 Myth #5: “Education Loan Means Guaranteed Job After Studies”

The Truth:

Education loans support learning — not job placement.

The bank funds you based on:

✔ University reputation

✔ Course potential

✔ Co-applicant’s financial profile

Whether you get a job depends entirely on:

◻ Skills

◻ Performance

◻ Market conditions

A loan covers fees — not your future career.

If you want to create AI Ads you can visit: https://adscribe.online

🔄 Myth #6: “Refinancing My Loan Is a Bad Idea”

The Truth:

Loan refinancing can be a smart financial decision if:

✔ You get a lower interest rate

✔ You want a longer tenure to reduce EMI

✔ You want to switch lenders for better terms

Refinancing is like upgrading your loan — many people save thousands by doing it.

🧍♂️ Myth #7: “Only Salaried People Can Get Loans”

The Truth:

Self-employed people can get loans — banks just need proof of:

✔ Income tax returns

✔ Business stability

✔ Revenue statements

Property owners, freelancers, and small business owners also qualify.

You just need the right financial documentation.

🚫 Myth #8: “You Should Never Take a Personal Loan”

The Truth:

Personal loans are unsecured (no collateral), so interest rates may be higher — but they are safe and fast if managed properly.

Advantages:

✔ No need to pledge assets

✔ Immediate approval

✔ Flexible usage

If taken for the right reasons and repaid responsibly, personal loans can help in emergencies or consolidating debt.

💳 Myth #9: “Credit Card Loans Are Always a Bad Choice”

The Truth:

They are expensive only if misused.

When are credit card loans helpful?

✔ 0% EMI offers

✔ Short-term borrowing you can repay quickly

✔ Emergency situations with no other funding source

The key is discipline and choosing the right repayment plan.

🕵️♂️ Myth #10: “Prepayment Is Always Free”

The Truth:

Many banks charge prepayment penalties to compensate for lost interest earnings.

Before closing a loan early, check:

✔ Prepayment fees

✔ Lock-in period

✔ Loan type

A loan with high penalty fees may not be worth prepaying.

🔍 Myth #11: “Low EMI Always Means a Better Loan”

The Truth:

Low EMI often means longer tenure, which means:

⬆ More interest over time

⬆ More total cost of the loan

Example:

| Loan | EMI | Tenure | Total Payment | Extra Cost |

|---|---|---|---|---|

| A | ₹15,000 | 5 Years | ₹9,00,000 | ₹2,00,000 |

| B | ₹10,000 | 8 Years | ₹9,60,000 | ₹2,60,000 |

Lower EMI can cost more overall. Balance affordability with interest efficiency.

💼 Myth #12: “You Can’t Get a Loan If You Have a Low Credit Score”

The Truth:

You can — but with:

⬆ Higher interest

⬆ Smaller loan amount

⬇ Lower tenure flexibility

Alternative options:

✔ Secured loans against property or gold

✔ Co-applicant loans

✔ NBFC lenders

✔ Credit score improvement plans

Low credit score doesn’t end your borrowing journey — it just changes the path.

⚠️ Myth #13: “Loan Insurance Is Useless”

The Truth:

Loan insurance can protect your family if:

✔ Borrower dies

✔ Serious illness occurs

✔ Permanent disability affects income

Loan insurance prevents financial burden during crisis situations.

It is especially important for home loans & education loans.

💰 Myth #14: “Home Loan Means I Fully Own My House”

The Truth:

Until you repay completely — the bank owns your property title.

You are the homeowner only after:

✔ Final EMI paid

✔ Lien removed

✔ Documents returned

Make sure to collect all original papers after loan closure.

🪙 Myth #15: “Gold Loans Are Only for Financially Weak People”

The Truth:

Gold loans are one of the cheapest and fastest borrowing methods.

✔ Very low interest rates

✔ Minimal paperwork

✔ Amount based on gold value

✔ Instant approval

Even wealthy business owners use gold loans to manage short-term liquidity.

You can also read our other loan related blogs, please visit: https://loans.fundicainvestments.com/loans-and-collateral/

🚧 Myth #16: “Taking Multiple Loans Is Always Bad”

The Truth:

Multiple loans are fine if:

✔ EMI ratio is below 40–50% of your income

✔ Credit score remains healthy

✔ Payments are never delayed

Businesses and homeowners often manage multiple loans with no issues.

🔄 Myth #17: “Loan Rejection Means I’ll Never Get Approved Again”

The Truth:

Rejection means you need to improve eligibility, such as:

✔ Credit score

✔ Income documentation

✔ Existing debt-to-income ratio

✔ Application accuracy

Loan approval is a process, not a one-time luck test.

📊 Myth #18: “Banks Always Give the Best Loans”

The Truth:

Sometimes NBFCs and online lenders offer:

⬇ Lower interest rates

⬇ Faster processing

⬆ Flexible criteria

Always compare options using:

✔ EMI calculators

✔ Annual Percentage Rate (APR)

✔ Total cost of borrowing

Smart borrowers shop for loans like they shop for phones.

🧠 Myth #19: “I Should Borrow the Maximum Amount Offered”

The Truth:

Just because the bank approves a high loan doesn’t mean you should take it.

Borrow as per your need and repayment ability, not temptation.

Too much loan = Long-term financial burden.

🎯 Myth #20: “A Loan Will Solve All My Financial Problems”

The Truth:

Loan is a tool to fulfill a goal, not a solution to poor money habits.

If someone takes a loan without a plan:

→ debt increases

→ expenses rise

→ stress grows

Loans support financial planning, not replace it.

⭐ How to Avoid Falling for Loan Myths

Before applying for any loan:

✔ Research and compare lenders

✔ Check credit score & improve if needed

✔ Understand fees, penalties, and fine print

✔ Choose tenure smartly

✔ Calculate total cost — not just EMI

✔ Borrow responsibly

Knowledge protects your money and peace of mind.

🏁 Final Conclusion

Loans are neither good nor bad —

➡ They become what you make them.

Believing popular loan myths can:

❌ increase costs

❌ reduce benefits

❌ damage financial health

But when you understand the truth:

✨ You borrow smartly

✨ You improve your credit score

✨ You achieve personal and business goals responsibly

Loans should empower your future — not complicate it.

Always make financially educated decisions, not fear-based ones.

Leave a Reply to Documents Needed for Different Types of Loans: Your Complete Guide to Getting Approved – Fundica Investments Cancel reply