Studying abroad is a dream for millions of students across the world. The idea of attending a globally ranked university, experiencing international culture, and building a successful global career is incredibly exciting. However, one reality often stands between students and their dreams — the cost of education abroad.

Tuition fees, living expenses, travel costs, insurance, and other charges can easily run into tens of thousands of dollars per year. For most families, paying this amount upfront is not practical. This is where study abroad education loans become a powerful financial solution.

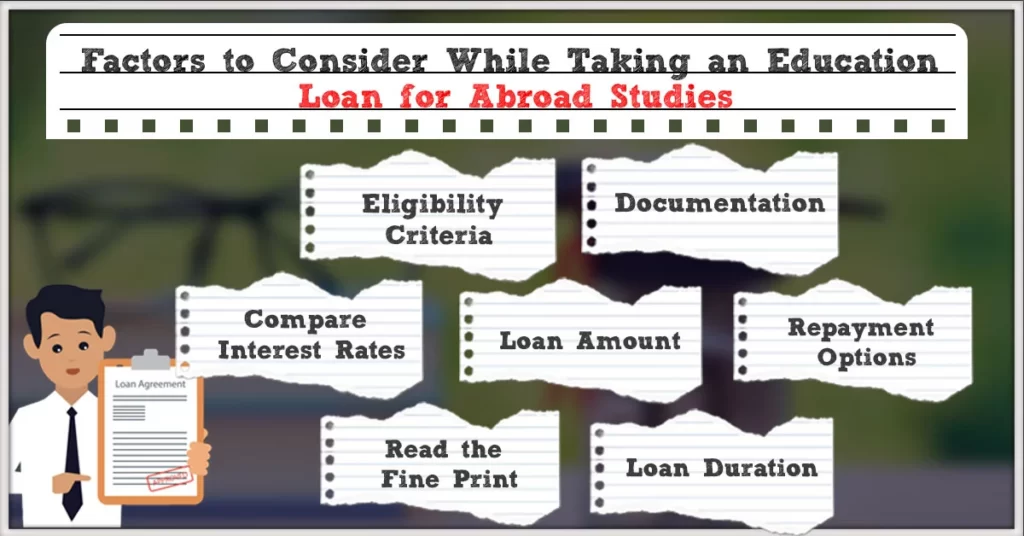

In this detailed guide, we will cover everything you need to know about education loans for studying abroad, including eligibility criteria, interest rates, repayment options, benefits, risks, and practical tips to secure the best loan.

Whether you’re planning to study in the USA, UK, Canada, Australia, Europe, or any other country, this guide will help you make an informed decision.

Table of Contents

- What Is a Study Abroad Education Loan?

- Why Education Loans Are Popular for Overseas Studies

- Types of Study Abroad Education Loans

- Secured vs Unsecured Education Loans

- Eligibility Criteria for Study Abroad Education Loans

- Eligibility for Students

- Eligibility for Co-Applicants

- Courses Covered Under Education Loans

- Countries Covered Under Study Abroad Loans

- Expenses Covered by Education Loans

- Interest Rates on Study Abroad Education Loans

- Factors That Affect Education Loan Interest Rates

- Fixed vs Floating Interest Rates

- Education Loan Amount — How Much Can You Borrow?

- Margin Money Explained

- Repayment Period & Moratorium

- Step-by-Step Process to Apply for a Study Abroad Loan

- Documents Required for Education Loans

- How to Improve Education Loan Approval Chances

- Education Loan Tax Benefits

- Common Mistakes to Avoid While Taking a Study Abroad Loan

- Pros & Cons of Education Loans for Abroad Studies

- FAQs on Study Abroad Education Loans

- Final Verdict: Is an Education Loan Worth It?

1. What Is a Study Abroad Education Loan?

A study abroad education loan is a financial product offered by banks and financial institutions to help students fund their overseas education. The loan covers tuition fees and related expenses, which the student repays in monthly installments after completing studies.

In simple terms:

An education loan allows you to study now and pay later, once you start earning.

Unlike personal loans, education loans usually offer:

- Lower interest rates

- Flexible repayment terms

- A moratorium period

- Tax benefits

If you want to create AI Ads you can visit: https://adscribe.online

2. Why Education Loans Are Popular for Overseas Studies

Studying abroad is expensive, and education loans make it accessible to a wider range of students.

Key Reasons Students Choose Education Loans:

- High cost of foreign education

- Limited scholarships and grants

- Ability to spread costs over several years

- Lower interest compared to personal loans

- No immediate repayment pressure

Education loans empower students to invest in their future without exhausting family savings.

3. Types of Study Abroad Education Loans

Education loans for studying abroad can broadly be divided into two categories:

1. Secured Education Loans

These loans require collateral, such as:

- Property

- Fixed deposits

- Insurance policies

They usually offer:

- Lower interest rates

- Higher loan amounts

- Longer repayment tenure

2. Unsecured Education Loans

These loans do not require collateral but depend heavily on:

- Student’s academic profile

- University ranking

- Co-applicant’s income and credit score

Interest rates are usually higher compared to secured loans.

4. Secured vs Unsecured Education Loans

| Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Collateral | Required | Not required |

| Interest Rate | Lower | Higher |

| Loan Amount | Higher | Limited |

| Approval | Easier | Stricter |

| Risk | Lower for lender | Higher for lender |

5. Eligibility Criteria for Study Abroad Education Loans

Eligibility criteria vary by lender, but most banks and NBFCs follow similar guidelines.

6. Eligibility for Students

Most lenders require students to meet the following conditions:

- Indian citizen (or resident as per lender policy)

- Confirmed admission to a recognized foreign university

- Age usually between 18–35 years

- Strong academic background

- Course should be job-oriented or professional

Universities with strong global rankings significantly improve approval chances.

7. Eligibility for Co-Applicants

Education loans almost always require a co-applicant, usually:

- Parent

- Guardian

- Spouse

Co-applicant eligibility includes:

- Stable income source

- Good credit history

- Ability to repay loan if student is unable to

The co-applicant’s financial strength plays a major role in loan approval.

8. Courses Covered Under Education Loans

Most lenders cover the following courses:

- Undergraduate programs

- Postgraduate programs

- MBA, MS, MTech

- Medical and healthcare courses

- Law courses

- STEM programs

- Professional and technical courses

Short-term or non-recognized courses may not be eligible.

9. Countries Covered Under Study Abroad Loans

Education loans are available for studies in:

- USA

- Canada

- UK

- Australia

- Germany

- France

- Ireland

- Singapore

- New Zealand

- Other recognized countries

Loan terms may vary depending on the country and university ranking.

10. Expenses Covered by Education Loans

A study abroad education loan typically covers:

- Tuition fees

- Hostel or accommodation charges

- Living expenses

- Travel expenses

- Examination fees

- Study materials

- Laptop (in some cases)

- Insurance premium

This comprehensive coverage reduces financial stress during studies.

11. Interest Rates on Study Abroad Education Loans

Interest rates vary widely based on lender type and loan structure.

Typical Interest Rate Range:

- Public sector banks: 8% – 11%

- Private banks: 9% – 13%

- NBFCs: 11% – 15%

Secured loans usually have lower rates than unsecured loans.

12. Factors That Affect Education Loan Interest Rates

Several factors determine the interest rate offered:

- Type of lender

- Presence of collateral

- Credit score of co-applicant

- University ranking

- Course type

- Loan amount

A strong academic and financial profile can help secure better rates.

13. Fixed vs Floating Interest Rates

Fixed Interest Rate:

- Rate remains constant

- EMI remains predictable

- Slightly higher interest

Floating Interest Rate:

- Rate changes with market conditions

- EMI may increase or decrease

- Generally lower than fixed rates

Floating rates are more common for education loans.

14. Education Loan Amount — How Much Can You Borrow?

Loan amount depends on:

- Course cost

- University reputation

- Country of study

- Type of loan

Typical loan limits:

- Secured loans: Up to ₹1.5 crore (or more)

- Unsecured loans: ₹20–50 lakhs

15. Margin Money Explained

Margin money refers to the portion of expenses the student must fund themselves.

Example:

- Total course cost: ₹40 lakhs

- Loan sanctioned: ₹36 lakhs

- Margin money: ₹4 lakhs

Margin money usually ranges between 5%–15%.

16. Repayment Period & Moratorium

Moratorium Period:

- Course duration + 6–12 months

- No EMI payment required

- Interest may accrue

Repayment Tenure:

- Typically 10–15 years

- Longer tenure = lower EMI

Early repayment is usually allowed.

17. Step-by-Step Process to Apply for a Study Abroad Loan

Step 1: Get University Admission

Secure a confirmed offer letter.

Step 2: Estimate Total Cost

Include tuition, living, and travel costs.

Step 3: Compare Lenders

Compare interest rates, fees, and repayment terms.

Step 4: Prepare Documents

Academic, financial, and identity documents.

Step 5: Submit Application

Apply online or offline.

Step 6: Loan Approval & Disbursement

Funds are released as per requirement.

18. Documents Required for Education Loans

- Admission letter

- Academic certificates

- KYC documents

- Income proof of co-applicant

- Bank statements

- Collateral documents (if applicable)

19. How to Improve Education Loan Approval Chances

- Apply early

- Choose reputed universities

- Maintain good academic record

- Ensure co-applicant has strong income

- Keep credit score high

- Provide complete documentation

20. Education Loan Tax Benefits

Under Section 80E, borrowers can claim tax deduction on:

- Entire interest paid

- For up to 8 years

This significantly reduces the effective loan cost.

21. Common Mistakes to Avoid While Taking a Study Abroad Loan

- Borrowing more than required

- Ignoring interest during moratorium

- Not comparing lenders

- Overlooking hidden charges

- Choosing longer tenure blindly

22. Pros & Cons of Education Loans for Abroad Studies

Pros:

- Makes global education affordable

- Lower interest than personal loans

- Flexible repayment

- Tax benefits

Cons:

- Long-term debt

- Interest accumulation

- Dependency on post-study employment

You can also read our other loan related blogs, please visit: https://loans.fundicainvestments.com/car-loan-refinancing-when-and-why/

23. Frequently Asked Questions (FAQs)

Is collateral mandatory for education loans abroad?

No, but unsecured loans have higher interest.

Can I repay loan early?

Yes, most lenders allow prepayment.

Do I need a job offer to repay?

No, but employment improves repayment ability.

24. Final Verdict: Is a Study Abroad Education Loan Worth It?

A study abroad education loan is not just debt — it’s an investment in your future.

If chosen wisely, with:

- A reputed university

- Strong career prospects

- Realistic repayment plan

…it can unlock opportunities that may otherwise remain out of reach.

Bottom Line:

Borrow responsibly, study smart, and repay strategically.

Leave a Reply